Many advisors have never heard of staging assets, which are kind of a step between your commissionable (your transactional) type of transactions versus your AUM (your recurring revenue) type of transactions. What these staging assets or staging transactions really do is sometimes provide you with true recurring revenue depending upon the vehicle that you use. But more importantly, they stage you to get all of the AUM, all of the rest of the portfolio, that therefore generates recurring revenue.

Here's the deal: fixed index annuities can be perfectly married together as staging assets. So if you are operating on the 4% rule (where you're just peeling off 4% from the top of the bucket of assets, with the idea that interest, dividends, growth, and so on will support that) or if you're living/managing off the 4% rule, this will help you. If you are operating with bond portfolios, and doing the 60/40 and various other things, I think this will also help you. The fixed index annuities, however, are really there, in this particular instance, to drive the income during retirement.

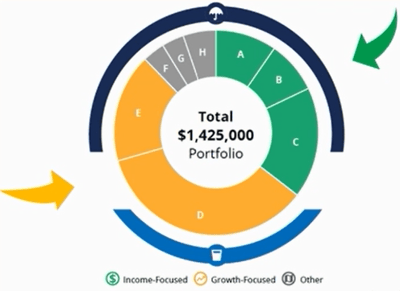

Now, here what we're showing is a view from the Asset Cycle Portfolio System, just one small graphic that we use inside of that system. What we're doing is this first account right up here in the top, labeled as A, is there to provide the first five years of retirement income. Let's assume these people are five years away from retirement right now. That first account, we're going to stage it right now. So it is going to sit in deferral for five years, and then five years from now they're going to trigger out five years worth of income, and it's going to pull those first five years of retirement income. Then, account B is going to pull the second five years of retirement income. So net, that will be a total of 10 years between those two. And it's starting five years in the future. So essentially, we're now 15 years into the future, right? So five years deferral, five years income, another five years income, and then account C - that's going to take them through the next subsequent 10 years of retirement income. So now I've got a total of 20 years of income spanned over 25 years from the moment I met them, because I'm assuming they're five years away from retirement.

Now, here what we're showing is a view from the Asset Cycle Portfolio System, just one small graphic that we use inside of that system. What we're doing is this first account right up here in the top, labeled as A, is there to provide the first five years of retirement income. Let's assume these people are five years away from retirement right now. That first account, we're going to stage it right now. So it is going to sit in deferral for five years, and then five years from now they're going to trigger out five years worth of income, and it's going to pull those first five years of retirement income. Then, account B is going to pull the second five years of retirement income. So net, that will be a total of 10 years between those two. And it's starting five years in the future. So essentially, we're now 15 years into the future, right? So five years deferral, five years income, another five years income, and then account C - that's going to take them through the next subsequent 10 years of retirement income. So now I've got a total of 20 years of income spanned over 25 years from the moment I met them, because I'm assuming they're five years away from retirement.

So, I'm simply taking a portion of the portfolio and designating it up front with these staging assets (staging for their ultimate retirement income). I like to use guaranteed vehicles - that's why I prefer the fixed indexed annuities, because I want to lock in and know exactly what's happening there. I've just given myself, in this example, 25 years as a financial advisor, to then take over all the rest of their equity portfolio. Now, if I can't make that thing stand up and sing over a 25-year period, I've got some real problems. But what I've done both for me and for the investor is, I have essentially put time on their side.

Just to give you a quick example from the S&P 500: this chart is about a 26 year span, from 1997 through 2023. And the red vertical lines indicate 10 year blocks. Now, if you give me 25 years as a financial advisor, I pretty much can't help but win. Now, if you block that down, like in the 'Lost Decade' - if somebody retired at the beginning of that decade, and then they came to you right at the end of that decade and needed to draw income, that's a tough conversation. This is why we like risk managed vehicles, because we can flatten out some of these troughs. And we can try to essentially eliminate that lost decade that's taken place.

Just to give you a quick example from the S&P 500: this chart is about a 26 year span, from 1997 through 2023. And the red vertical lines indicate 10 year blocks. Now, if you give me 25 years as a financial advisor, I pretty much can't help but win. Now, if you block that down, like in the 'Lost Decade' - if somebody retired at the beginning of that decade, and then they came to you right at the end of that decade and needed to draw income, that's a tough conversation. This is why we like risk managed vehicles, because we can flatten out some of these troughs. And we can try to essentially eliminate that lost decade that's taken place.

But, if I've got 25 years of time, you can't find a period of time in the history of the stock market that you would not look good over a 25-year period. So, buying time to get the rest of the portfolio and then investing it wisely and accordingly for long-term growth... I can only do that if I start first with staging assets. And personally, I would recommend using fixed index annuities for that section A, B, and C in the chart above.

Now, if you're interested, we have a new, free report called the 'Advisor's 12-Step Reset for Predictable Growth, Value & Lifestyle'. It's a smooth, 12-step process that I've uncovered and discovered over my 35+ year journey in this industry. And it's designed to generate a predictable practice with automated revenue and lifetime rewards.

--

The RARE Advisor is a business model supercharged by Recurring And Repeatable Events. With more than thirty years of working with and coaching successful advisors, host Mike Walters (along with other leaders in the industry), discusses what it takes to grow a successful practice. With the aim of helping financial professionals and financial advisors take their business to the next level, Mike Walters shares insights and success stories that make a real impact. Regardless of the stage of your practice, The RARE Advisor will provide thoughtful guidance, suggestions for developing systems and processes that work, and ideas for creating an authentic experience for your clients.

The RARE Advisor is also a podcast! Subscribe today via Apple Podcasts, Google Podcasts, or your preferred podcast listening service for easier on-the-go listenin

Author Info

Mike Walters is the Chief Executive Officer (CEO) of USA Financial, leading the firm since its inception in 1988. Mike is committed to...

Related Posts

Why Great Advisors Manage Expectations Before They Manage Portfolios

What if one of the most important promises a financial advisor could make is that they'll eventually lose a client money? In this episode of the Financial Advisor Marketing Playbook, Mark Mersman sits down with Josh Kneller of Atlas Capital Management to discuss investor behavior, managing expectations, market volatility, and advisor communication. Josh shares why advisors should stop chasing performance, start preparing clients for inevitable downturns, and focus on becoming a trusted opportunity rather than a salesperson. From handling difficult conversations to building stronger client relationships, this episode offers practical insights for advisors looking to improve retention, referrals, and long-term growth.

.png)

Financial Advisors: Will Your Clients’ Children Keep You?

Most advisors recognize the importance of multi-generational planning, but very few have a repeatable process to build relationships with clients' children and grandchildren before a major life event occurs. In this episode of The Rare Advisor, Aaron Grady breaks down the Family Phone Call process step-by-step, including how to introduce the idea, schedule the call, involve next-generation advisors, follow up effectively, and track success over time. Learn how this simple but powerful framework can strengthen client relationships, reduce retention risk, support succession planning, and create long-term enterprise value for your firm.

What Financial Advisors Can Learn From Disney About Creating Memorable Client Experiences

What can financial advisors learn from Disney? In this episode of the Financial Advisor Marketing Playbook, Mark Mersman sits down with former Disney leader and customer experience expert Vance Morris to discuss how advisors can create memorable client experiences that drive loyalty, referrals, and retention. From Disney's obsession with detail and service recovery to creating anticipation, reducing friction, and building emotional connections, Vance shares practical strategies advisors can implement immediately to elevate their client experience and stand apart from competitors.